Feb 23 (CNN) – Global stock markets tumbled and crude oil prices surged to $99 per barrel on Tuesday after Russia ordered troops into parts of eastern Ukraine.

European markets dropped in early trading. The FTSE 100 (UKX) dipped 0.4% in London, while France’s CAC 40 (CAC40) shed 0.8%. Germany’s DAX (DAX) tumbled 1.4%. Russian stocks dropped 6.9%, after crashing more than 10% Monday, and the ruble weakened against the dollar for the fourth consecutive trading session.

Subscribe to our Telegram channel for the latest updates from around the world

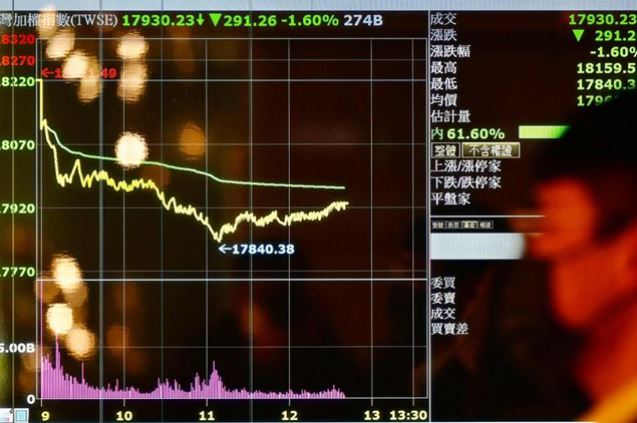

Japan’s Nikkei 225 (N225) fell 1.7%, while China’s Shanghai Composite (SHCOMP) dropped 1%. Hong Kong’s Hang Seng Index (HSI) fell 2.7%, its biggest daily loss in five months.

Wall Street was also headed lower as traders return from the holiday weekend. Dow (INDU) futures dropped 1.4%. S&P 500 futures were down 1.3%, while Nasdaq futures shed 2.1%.

READ: Putin lays claim to the whole of Ukraine

Russian President Vladimir Putin has ordered Russian troops into two separatist pro-Moscow regions in eastern Ukraine after recognizing their independence on Monday. The move appears to be the opening salvo of a larger potential military operation targeting Ukraine, US and western officials told CNN.

“It feels like the situation can dramatically escalate at any moment and that’s going to keep investors on edge for now,” wrote Craig Erlam, senior market analyst at Oanda, in a research note on Tuesday. “We may well be on the brink of something terrible happening and that’s continuing to feed into the negativity in the markets,” he added.

READ: Britain to impose financial sanctions on Russia as it has begun invading Ukraine

Oil surges

Escalating uncertainty about Ukraine was reflected by a spike in energy prices. US crude futures jumped 5.4% to trade at $95.65 per barrel. Brent crude, the global benchmark, surged 3.8% to $99.17 per barrel.

Russia is one of the world’s biggest producers of oil. It is also a major exporter of natural gas.

Investors fear that conflict in Ukraine could limit or stop the flow of Russian gas into Europe, making it much more expensive for people to heat and light their homes. In 2020, Russia accounted for about 38% of the European Union’s natural gas imports, according to data agency Eurostat.

READ: Ukraine wants peace but won’t give up its land to Russia, president says

The region’s biggest economy, Germany, is particularly exposed as it weans itself off of coal and nuclear power. So are Italy and Austria, which receive gas via pipelines that run through Ukraine.

Western countries would likely respond to a Russian invasion of Ukraine with punishing sanctions that could cut Russian banks off from the global financial system and make it more difficult for the country to export its oil and gas.

Chinese tech stocks hammered

Worries about a renewed tech crackdown by Beijing also dealt a blow to some of the biggest Chinese companies in the sector on Tuesday.

The Hang Seng Tech Index, which tracks 30 largest tech companies listed in the city, lost 1.9%, down for a third day in a row.

On Friday, Chinese authorities released new rules ordering food delivery platforms to cut service fees they charge businesses. Online food delivery platform Meituan fell 5% on Tuesday. The stock has plunged 23% since Friday.

Alibaba Group (BABA), which owns food-delivery platform Ele.me, dropped 3%. Social media and gaming giant Tencent (TCEHY) fell as much as 3%. It closed down 0.1%. The firm also holds a major stake in Meituan.

For similar articles, join our Telegram channel for the latest updates. – click here